Construction Bonds

Explained

Construction Bonds Explained

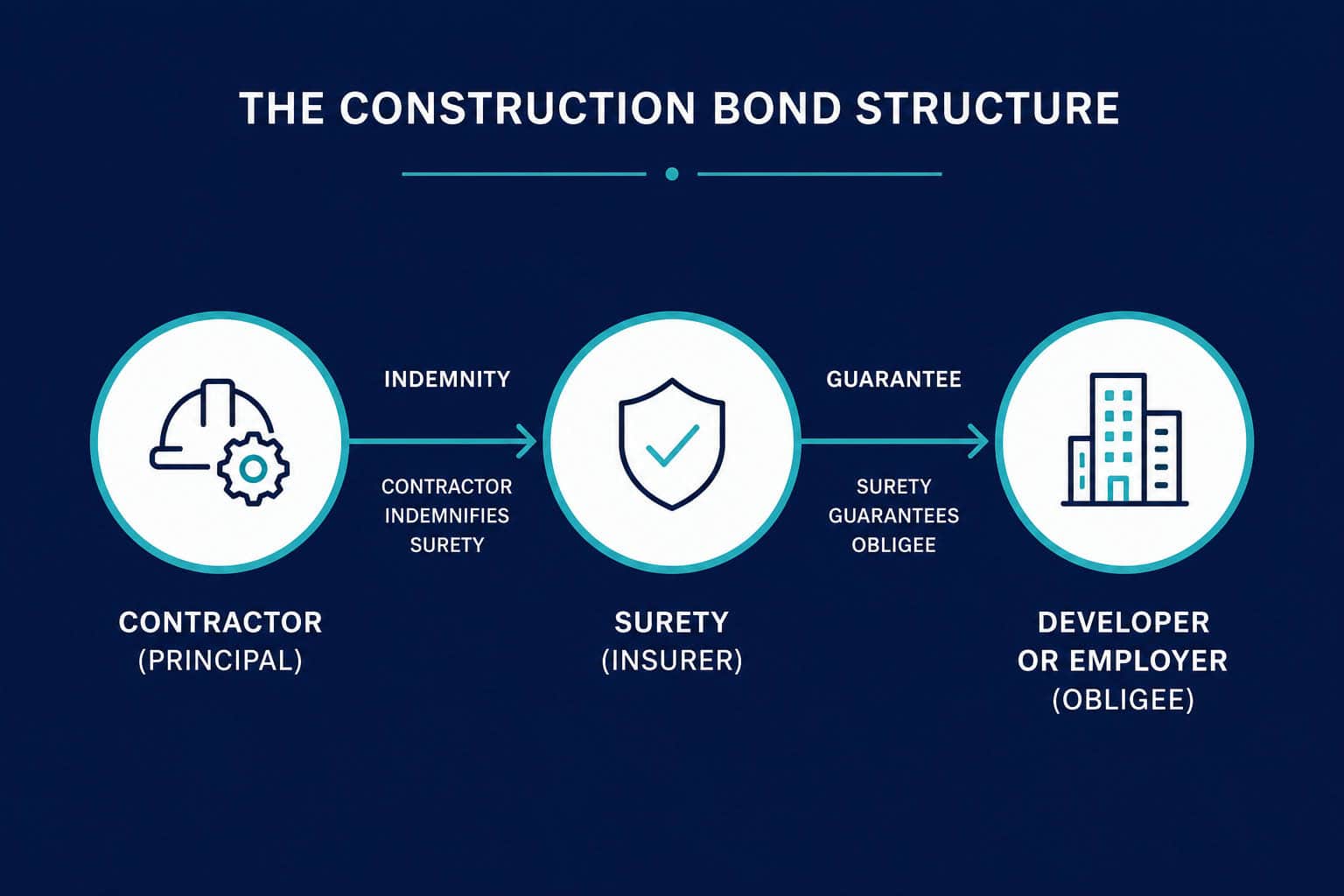

A construction bond is a financial guarantee issued by a surety on behalf of a contractor in favour of a developer or employer. It protects the beneficiary if the contractor fails to meet its contractual obligations. A construction bond involves three parties: the contractor who provides the bond, the surety who guarantees it, and the developer or employer who benefits from it.

In the UK market, construction bonds are commonly used on medium and large developments to manage performance risk, protect advance payments and satisfy lender or planning requirements. They are distinct from insurance and operate under different legal and commercial principles.

This page explains what construction bonds are, how they work, when they are required and how to approach them strategically.

The three parties in a construction bond

Every construction bond involves three defined parties:

- Principal – the contractor whose obligations are being guaranteed

- Obligee – the developer, employer or beneficiary protected by the bond

- Surety – the insurer or financial institution issuing the bond

If the contractor fails to meet its contractual obligations, the beneficiary may make a claim against the bond, subject to its terms. The surety may then seek recovery from the contractor under an indemnity agreement.

This tripartite structure is fundamental. It distinguishes bonds from insurance and explains why bond underwriting focuses heavily on contractor financial strength.

Construction bonds vs insurance: the key difference

Construction bonds are frequently confused with insurance. They are not the same.

A bond guarantees performance of a contractual obligation. Insurance protects against defined risks such as property damage or liability claims.

The structural difference is important:

If a performance bond is called due to contractor default, the surety pays the beneficiary in accordance with the bond wording. The surety then has recourse to the contractor. With insurance, the insurer absorbs the insured loss.

This distinction affects underwriting, pricing and the willingness of providers to offer cover. It also explains why contractor financial stability is central to bond availability.

For a deeper explanation of how bonds differ from insurance, see our article on how they differ from insurance.

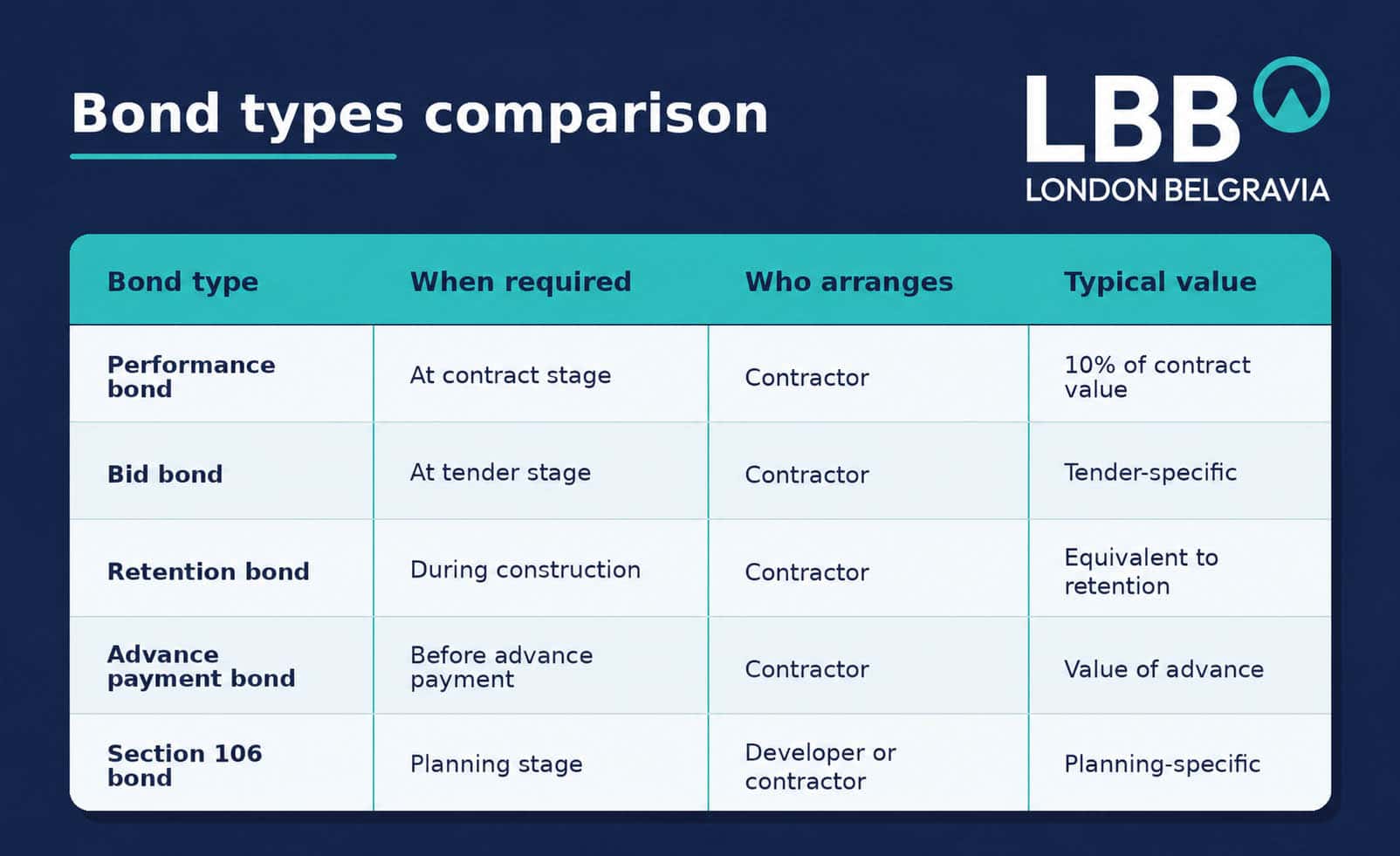

Types of construction bond used in the UK

Five core bond types are commonly used on UK construction projects. Each addresses a different risk within the development lifecycle.

Peformance Bonds

A performance bond protects the developer if a contractor fails to complete the works in accordance with the building contract.

In the UK, performance bonds are typically set at 10% of the contract value. They are usually required under standard forms such as JCT where the employer elects to include the provision.

Performance bonds are most common on projects over £1m in value, particularly where lenders are involved or where contractor insolvency risk is a concern.

For detailed guidance, see our page on performance bonds.

BID bonds

A bid bond provides assurance during the tender stage. It protects the employer if a contractor withdraws its bid or fails to enter into the contract after being appointed.

Bid bonds are more common on public or large commercial tenders, particularly where procurement rules require evidence of financial commitment.

They are less frequently used in smaller private developments but remain relevant where tender integrity is critical.

Retention bonds

Under many contracts, the employer retains a percentage of each interim payment to protect against defects. A retention bond allows the contractor to receive the retained cash while providing equivalent security to the employer.

This can improve contractor cash flow while preserving protection for the developer.

Retention bonds are often used on larger projects where cash flow pressures are material or where negotiation between employer and contractor supports alternative security arrangements.

Advance Payment Bonds

Where a developer makes a significant advance payment for materials, off-site manufacture or mobilisation, an advance payment bond protects that sum.

If the contractor fails to perform, the bond provides a mechanism for recovery of the advance.

Advance payment bonds are particularly relevant on projects involving specialist packages, modular construction or significant upfront procurement costs.

Section 106 Bonds

Section 106 bonds are linked to planning obligations. They provide financial security to a local authority that specified works or contributions will be delivered.

These bonds are typically required under planning agreements and are separate from building contract security.

They are common on residential and mixed-use schemes with infrastructure, affordable housing or public realm obligations.

Conditional vs on-demand bonds

One of the most important distinctions in UK practice is between conditional and on-demand bonds.

Conditional vs on-demand bonds

A conditional bond requires the beneficiary to demonstrate contractor default before a valid claim can be made. The surety’s liability is linked to proof of breach under the building contract.

In the UK, performance bonds are typically conditional. This reflects a balanced allocation of risk between employer and contractor.

Conditional wording often limits exposure to demonstrable loss, subject to the bond cap.

on-demand bonds

An on-demand bond allows the beneficiary to call the bond without proving default, provided the demand complies with the bond wording.

These instruments are more common on international projects and infrastructure schemes. In the UK private development market, contractors generally resist on-demand wording because it creates immediate payment exposure regardless of dispute.

When reviewing bond documentation, you should understand clearly whether the instrument is conditional or on-demand. The wording materially affects risk.

When is a construction bond required?

Construction bonds are not automatic. They are triggered by contractual, funding or regulatory requirements.

1. Required by contract

Standard forms such as JCT include optional provisions for performance bonds. The employer may require one as a condition of appointment. This decision is often driven by project size, contractor strength and risk appetite.

2. Required by a lender or funder

Lenders increasingly require performance bonds on projects valued over £1m. This is particularly common where development finance is involved. In 2025, rising contractor insolvencies led to greater scrutiny of contractor financial stability. As a result, bonds are now being required on schemes that might previously have proceeded without them. A lender’s requirement is separate from the building contract but must align with it. Bond wording should reflect contractual risk allocation.

3. Required under planning conditions

Section 106 obligations often require financial security. A section 106 bond may be required before commencement or occupation. These arrangements sit outside the main building contract and require coordination between legal, planning and insurance advisors.

What is the bond value for a performance bond?

In the UK market, performance bonds are typically set at 10% of the contract value.

This does not mean that the employer will automatically receive 10% if the bond is called. Payment is subject to the bond wording and evidence of loss.

The 10% figure represents a cap on the surety’s liability. It is designed to provide meaningful protection without making the bond commercially prohibitive.

How much does a construction bond cost?

The cost of a construction bond depends on:

- Contractor financial strength

- Project size and complexity

- Bond wording

- Duration

- Market conditions

For performance bonds, pricing to the contractor is commonly in the range of 0.5%–2% of the bond value. This is not a fixed rate and should not be treated as such.

The contractor usually pays for the bond, and the cost is typically reflected within the tender price.

Following the increase in contractor insolvencies during 2025, underwriting scrutiny has tightened in some parts of the market. Contractors with weaker balance sheets may face higher pricing or reduced capacity.

Accurate pricing requires engagement with A-rated sureties and a clear presentation of financial information.

Who pays for a construction bond?

In most cases, the contractor pays for the bond. The premium forms part of the contractor’s overhead and is factored into its tender.

From a developer’s perspective, the bond is therefore indirectly funded through the contract sum.

Where bonds are required by lenders or planning authorities, the obligation still usually falls on the contractor unless negotiated otherwise.

Can a contractor with a poor credit history obtain a bond?

Bond underwriting is credit-driven. Sureties assess financial statements, order books, past performance and liquidity.

A contractor with weak financials may still obtain a bond, but:

- Pricing may be higher

- Capacity may be limited

- Additional security may be required

In some cases, the market may not support the required bond at all. This can affect project viability.

Early engagement is critical. Leaving bond procurement until immediately before contract execution can create delay.

What happens when a bond is called?

If a contractor defaults, the beneficiary may issue a claim in accordance with the bond wording.

For a conditional bond, this usually requires evidence of breach and loss. The surety will assess the claim against the bond terms.

If the claim is valid, the surety pays the beneficiary up to the bond cap. The surety then seeks recovery from the contractor under the indemnity agreement.

Bond calls are serious events. They often arise in parallel with insolvency or formal dispute.

Understanding the claims process in advance is part of prudent risk management.

How long does a construction bond last?

Bond duration depends on its purpose.

- Performance bonds usually run until practical completion or expiry of the defects period

- Retention bonds mirror the retention release timetable

- Advance payment bonds typically reduce as payments are certified

- Section 106 bonds run until planning obligations are discharged

Duration should align with the underlying contractual risk.

When do you need a construction bond?

You may need a construction bond if:

- Your building contract requires one

- Your lender mandates one

- Your planning agreement requires financial security

- You are making significant advance payments

- You are concerned about contractor insolvency risk

The decision is not purely mechanical. It is strategic.

A bond changes the risk profile of your project. It may improve lender confidence and reduce exposure to contractor failure. It also increases contractor cost and may affect tender appetite.

Balancing these factors requires informed judgement.

Using the same provider for warranties and bonds

Developers often ask whether the same insurer can provide both a structural warranty and a performance bond.

In some cases, yes. In others, no.

Structural warranties and bonds are distinct instruments with different underwriting criteria. Warranty providers assess technical construction risk. Sureties assess contractor financial strength.

Using the same provider may streamline administration but should not override considerations of credit rating, capacity and bond wording.

LBB advises across both warranties and bonds, ensuring that security arrangements are coherent rather than fragmented.

Why use an independent advisor to arrange a bond?

The UK bond market is not uniform. Providers differ in appetite, credit rating, wording and capacity.

An independent advisor provides access to the whole market rather than a single surety.

A-rated insurers matter

LBB works only with A-rated insurers. This protects the developer in the event of a claim being made on the bond. The financial strength of the surety is central to the value of the instrument.

A bond from a weak provider may satisfy a contractual requirement on paper but offer limited practical protection.

Market access and negotiation

Bond wording is not always standard. Conditional clauses, notice provisions and liability caps require careful review.

LBB’s role is advisory. We do not simply source quotes. We help you determine:

🞗 Which bond is required

🞗 Whether the wording is appropriate

🞗 Whether the provider is financially robust

🞗 How the bond aligns with the building contract

In a market affected by contractor insolvencies and tightening underwriting standards, this advisory layer is increasingly important.

Contact Us

Contact UsFrequently asked questions

Who pays for a construction bond?

The contractor usually pays for the bond, with the cost reflected in the contract sum.

What happens when a bond is called?

The beneficiary submits a claim under the bond wording. If valid, the surety pays up to the bond limit and seeks recovery from the contractor.

Can I use the same provider for my structural warranty and my performance bond?

Sometimes, but not always. The decision should be based on credit strength, underwriting appetite and wording, not administrative convenience.

How long does it take to arrange a construction bond?

Timing depends on contractor financial information and project complexity. For established contractors with strong financials, bonds can often be arranged within a few weeks. For complex or high-value schemes, early engagement is advisable to avoid delay.

Independent advice on construction bonds

Construction bonds sit at the intersection of contractual risk, financial strength and project delivery.

They are not simply a tick-box requirement. The choice of provider, wording and structure affects lender confidence, contractor appetite and downstream risk.

LBB provides whole-of-market independent advice across performance bonds, bid bonds, retention bonds, advance payment bonds and section 106 bonds. You do not need to approach separate providers for each instrument.

If you have been asked to provide or obtain a bond, or you are reviewing risk on a forthcoming development, we can advise on the appropriate structure and source it from A-rated insurers.

To discuss which bond is required for your project and how it should be structured, speak with LBB’s specialist team.